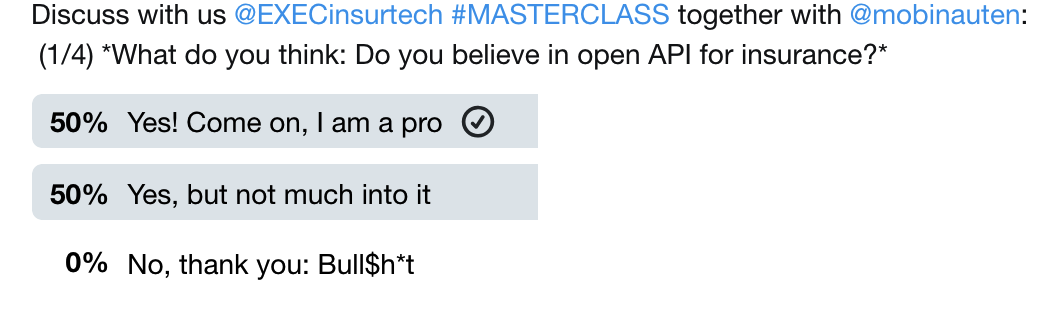

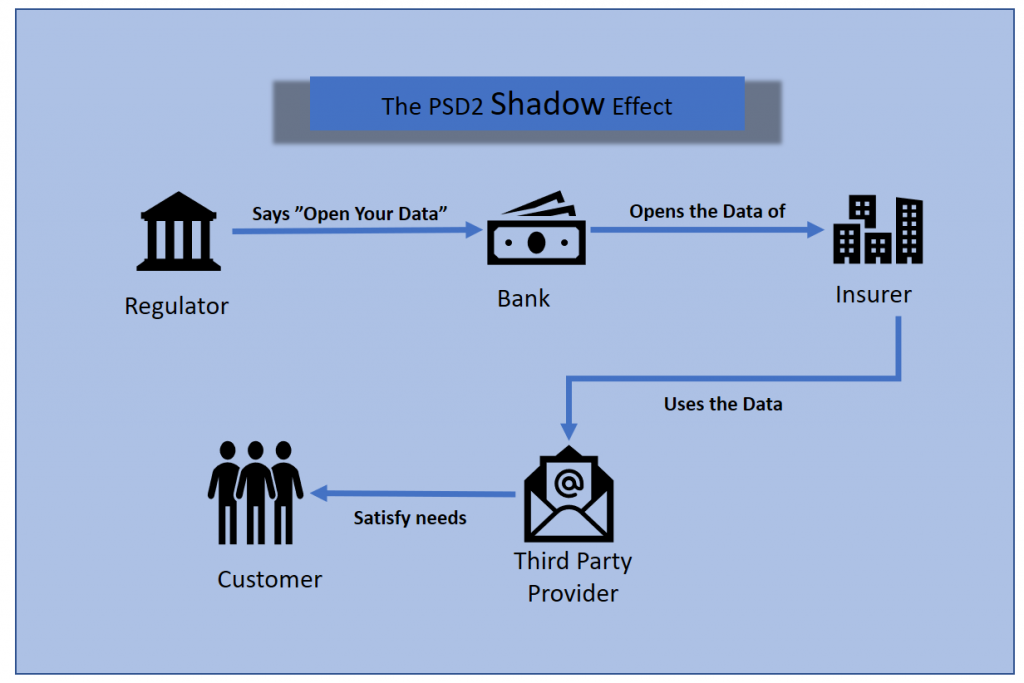

When Regulator says Open Your Data to the Banks, the Insurers have to listen

The new customer, the Digital Native wants to work digitally, wants to compare and wants usually all (basic) financial information in one digital view.

His ‘Internet shaped DNA’ doesn’t understand and in the long run will not tolerate offline traditions and patterns of classical incumbents, I assume.

Two of these customer needs have already been the base of a lot of successful inventions and startups in the past years.

All of us working in the insurance sector know and respect the power of digital aggregators. Since some years the customer can now work digitally and compare. What still wasn’t satisfied is the need of

Consolidated Digital Views.

Some startups in the last years tried to fulfill this requirement, with more or less average success. Far away from the success of implementing the Digital and Comparing Capability.

But times might change now. The ‘

Digital Insurance Folder Idea‘ gets a second chance with PSD2, I think.

Gone are the Days

With the PSD2 directive the regulator

tells the banks to open their data. But not only open ‘their’ data, but to open a lot of customer data and subsequently also a lot of insurance data. Third Parties, Startups and also traditional incumbents can now satisfy the third basic need of the customer:

The one place for all their insurance data. Automatically, with one click.

Gone are the days as the customer had to manually add his insurance data into web interfaces or activate long taking, in-transparent and risky manual data and account transportation processes.

Gone are the days as the legal situation was unclear and consequences unpredictable.

One might say it’s only the header data of the insurance contracts, but it’s an entry, a starting point. The days of the manual, error prone and complicated creation of

The One View are over now, if you ask me. With one click and some Machine Learning in the background!

Once the user has established a relationship with the new or old Third Party (activating the new third capability by linking his bank accounts) the steps to Detail Data, Contract Management, Change and New Business are minor ones, I predict.

In some years nobody will remember that one had to handle every insurance contract form different insurers differently.

What this means in terms of customer relationship, interactions and loyalty everybody has to find out on his own.

I’m just asking myself, if the regulator really has understood that he also opened implicitly the insurer’s data, when he forced the banks to become more open? Were the insurers allowed to have had an opinion in advance?