A lot of people are talking about ecosystems and platformeconomy. They assume platform heroes like Amazon and Google will disrupt their industry soon. Especially banks, but even more

the Insurers are fearing loosing their customer to the ‘High Engagement Heroes’.

Sensitive respect and awareness is justified and risks are real.

But this new digital war is not lost yet.

While GAFA might be the current world champion for customer engagement they aren’t yet the ‘Champion of Trust’ I believe.

Yes, Amazon is on its way to becoming the one. Amazon’s priority is to satisfying its customers, understood, trust is the base of any sustainable business.

But when you compare the ‘money-‘ and insurance-business with retail business today, ‘trust’ still has a different meaning.

So how can one survive this new ecosystem war?

Fight the trust battle!

Participate and build your own ecosystem and do what you can do best to play a sustainable, prefered and accepted role.

Be the most trusted partner for your customer and support him with (Digital) Trust Services. Base your new ecosystem on trust and fill in the gaps your government couldn’t fill in the years (see picture above – the unlucky und unsuccessful attempt to the create a government based Digital Identity in Germany).

Now it’s your chance to becoming the long awaited ecosystem of trust.

How can

Digital Trust look like?

One very interesting use case is to supporting 3rd party services with

onbording-, KYC-, registration-, authentication- and authorization-services.

A bank has the necessary customer data and usually a long relationship either. Digitalize these services via OpenAPIs and become an important part of, probably the most important one of a finance platformeconomy,

Compared with Google’s or Facebook’s social login, but with the regulatory quality, acceptance and reputation even the most demanding onboarding processes can be satisfied with. In Germany companies like

YES or

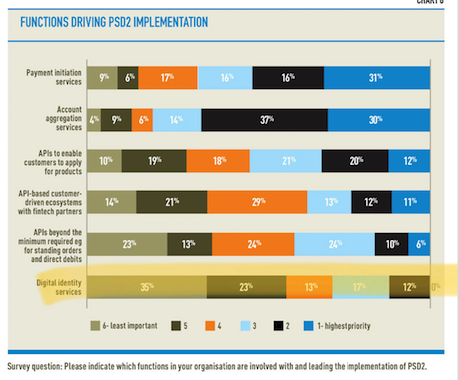

Verimi have already started implementing corresponding services and some banks and insurers have already acknowledged their contribution. But from a platform and CxO perspective this approach is still a very new and less popular one, as this statistic documents.

(Interesting Blog post about Digital Identities –

German)

Another Digital Trust use case is indeed the

good old payment and checkout process. Already a very mature digital process and provided by APIs and many parties (e.g Paypal or Paydirekt), but if provided together with the Digital Identity process banks and insurers could create a vertical touchpoint frame surrounding platform activities and services.

Compared with a room or building where you

‘own’ the save entry and exit. The customer always will pass both.

Fill the room with services and products the customer needs, not necessarily the ones you created, but which helps the customer most.

This is another important aspect of creating an Ecoystem of Trust. A good and recent example is the integration of

Friendsurance into the Deutsche Bank Retail portal.

Deutsche Bank owns the entry, the exit and provides an insurance comparison platform, not the one insurance product. Deuba provides what the customer is looking for, not what serves the bank most – selling the one insurance.

Revitalizing the very old Ecosystems of Trust – the banks and the insurers.

So how can one survive this new ecosystem war?

Fight the trust battle!

Participate and build your own ecosystem and do what you can do best to play a sustainable, prefered and accepted role.

Be the most trusted partner for your customer and support him with (Digital) Trust Services. Base your new ecosystem on trust and fill in the gaps your government couldn’t fill in the years (see picture above – the unlucky und unsuccessful attempt to the create a government based Digital Identity in Germany).

Now it’s your chance to becoming the long awaited ecosystem of trust.

How can Digital Trust look like?

One very interesting use case is to supporting 3rd party services with onbording-, KYC-, registration-, authentication- and authorization-services.

A bank has the necessary customer data and usually a long relationship either. Digitalize these services via OpenAPIs and become an important part of, probably the most important one of a finance platformeconomy,

Compared with Google’s or Facebook’s social login, but with the regulatory quality, acceptance and reputation even the most demanding onboarding processes can be satisfied with. In Germany companies like YES or Verimi have already started implementing corresponding services and some banks and insurers have already acknowledged their contribution. But from a platform and CxO perspective this approach is still a very new and less popular one, as this statistic documents.

So how can one survive this new ecosystem war?

Fight the trust battle!

Participate and build your own ecosystem and do what you can do best to play a sustainable, prefered and accepted role.

Be the most trusted partner for your customer and support him with (Digital) Trust Services. Base your new ecosystem on trust and fill in the gaps your government couldn’t fill in the years (see picture above – the unlucky und unsuccessful attempt to the create a government based Digital Identity in Germany).

Now it’s your chance to becoming the long awaited ecosystem of trust.

How can Digital Trust look like?

One very interesting use case is to supporting 3rd party services with onbording-, KYC-, registration-, authentication- and authorization-services.

A bank has the necessary customer data and usually a long relationship either. Digitalize these services via OpenAPIs and become an important part of, probably the most important one of a finance platformeconomy,

Compared with Google’s or Facebook’s social login, but with the regulatory quality, acceptance and reputation even the most demanding onboarding processes can be satisfied with. In Germany companies like YES or Verimi have already started implementing corresponding services and some banks and insurers have already acknowledged their contribution. But from a platform and CxO perspective this approach is still a very new and less popular one, as this statistic documents.

Today Oliver showed me an interesting article in faz.net, the online news platform of “Frankfurter Allgemeine Zeitung”, one of the big German newspapers. It reported that Allianz (Germany’s biggest insurance company) is requesting a trustee of data collected by cars. As the article mentions, this is because there is no agreement between different parties such as car manufacturers, vehicle inspectors, insurers and service stations about who will manage data continuously created by cars and how all the other parties will get access to them.

Allianz doesn’t want car manufacturers to collect and store data on their infrastructure and make them available to others afterwards. A trustee must collect and manage these data, Allianz requests. One of the main reasons Allianz brings according to this publication is that data collected by cars will become more important in case of accidents in which self driving cars are involved.

Well … wait a minute … a trustee? Seriously?

Haven’t we recently been discussing technologies, which make trustees obsolete? Is that a case for distributed ledger technologies (DLT)?

And yes, we think that DLT is exactly the technological answer to solve this issue of trust between all parties.

Using DLT there will be one network consisting of several peers each of which ran by one of those parties interested in the data. Of course cars themselves must be part of the network as well. They can be considered as clients accessing the network. While a car is going for a ride, it will collect data and send them to the network by invoking a so-called “transaction”.

Transactions are provided by smart contracts being part of the network and holding the business logic of it. This business logic is used to either write data into the ledger or read them from it. The Ledger can be considered as a database where all collected information will be stored.

Once a car calls a smart contract’s method to write data, they will be validated, signed and distributed to the network. A consensus algorithm will make sure that all peers will have the same valid and consistent data. As data are signed, hashed and blocked there will be no reason for an insurer to insist on having a “trustee of data”.

A DLT used for this case not only makes sure that all participants can trust each other without having a trustee in between, it may also help to create new use cases which not being thought about in the first place.

While we have been thinking about

Today Oliver showed me an interesting article in faz.net, the online news platform of “Frankfurter Allgemeine Zeitung”, one of the big German newspapers. It reported that Allianz (Germany’s biggest insurance company) is requesting a trustee of data collected by cars. As the article mentions, this is because there is no agreement between different parties such as car manufacturers, vehicle inspectors, insurers and service stations about who will manage data continuously created by cars and how all the other parties will get access to them.

Allianz doesn’t want car manufacturers to collect and store data on their infrastructure and make them available to others afterwards. A trustee must collect and manage these data, Allianz requests. One of the main reasons Allianz brings according to this publication is that data collected by cars will become more important in case of accidents in which self driving cars are involved.

Well … wait a minute … a trustee? Seriously?

Haven’t we recently been discussing technologies, which make trustees obsolete? Is that a case for distributed ledger technologies (DLT)?

And yes, we think that DLT is exactly the technological answer to solve this issue of trust between all parties.

Using DLT there will be one network consisting of several peers each of which ran by one of those parties interested in the data. Of course cars themselves must be part of the network as well. They can be considered as clients accessing the network. While a car is going for a ride, it will collect data and send them to the network by invoking a so-called “transaction”.

Transactions are provided by smart contracts being part of the network and holding the business logic of it. This business logic is used to either write data into the ledger or read them from it. The Ledger can be considered as a database where all collected information will be stored.

Once a car calls a smart contract’s method to write data, they will be validated, signed and distributed to the network. A consensus algorithm will make sure that all peers will have the same valid and consistent data. As data are signed, hashed and blocked there will be no reason for an insurer to insist on having a “trustee of data”.

A DLT used for this case not only makes sure that all participants can trust each other without having a trustee in between, it may also help to create new use cases which not being thought about in the first place.

While we have been thinking about

For an IT guy the last ten years have been very boring ones often as most IT Euros spent were regulation motivated.

The newest ones for example are

For an IT guy the last ten years have been very boring ones often as most IT Euros spent were regulation motivated.

The newest ones for example are

These kind of vertical ecosystems exist since decades – mutual societies and comparable organisations – but with the digital revolution currently happening everywhere there’s a new chance to reinvent and even to massively extend this model far beyond what was possible before.

And this is a chance for the old incumbents, the old banks and insurers to beat the GAFAs and all other coming platform revolutionaries and newbies on their home-turf.

They know their customers, they have build trust and relationship over the century. Now it’s time to modernize their houses and to copy the digital and platform services approaches. And to profile these much better than the global horizontal providers can.

You don’t need to own the product, you need to ‘own’ the customer and to provide trusted services via modern, simple and fast technologies. In the future you will very likely make more revenue with platform services and network effects than with a traditional approach as these

These kind of vertical ecosystems exist since decades – mutual societies and comparable organisations – but with the digital revolution currently happening everywhere there’s a new chance to reinvent and even to massively extend this model far beyond what was possible before.

And this is a chance for the old incumbents, the old banks and insurers to beat the GAFAs and all other coming platform revolutionaries and newbies on their home-turf.

They know their customers, they have build trust and relationship over the century. Now it’s time to modernize their houses and to copy the digital and platform services approaches. And to profile these much better than the global horizontal providers can.

You don’t need to own the product, you need to ‘own’ the customer and to provide trusted services via modern, simple and fast technologies. In the future you will very likely make more revenue with platform services and network effects than with a traditional approach as these