A lot of people are talking about ecosystems and platformeconomy. They assume platform heroes like Amazon and Google will disrupt their industry soon. Especially banks, but even more

the Insurers are fearing loosing their customer to the ‘High Engagement Heroes’.

Sensitive respect and awareness is justified and risks are real.

But this new digital war is not lost yet.

While GAFA might be the current world champion for customer engagement they aren’t yet the ‘Champion of Trust’ I believe.

Yes, Amazon is on its way to becoming the one. Amazon’s priority is to satisfying its customers, understood, trust is the base of any sustainable business.

But when you compare the ‘money-‘ and insurance-business with retail business today, ‘trust’ still has a different meaning.

So how can one survive this new ecosystem war?

Fight the trust battle!

Participate and build your own ecosystem and do what you can do best to play a sustainable, prefered and accepted role.

Be the most trusted partner for your customer and support him with (Digital) Trust Services. Base your new ecosystem on trust and fill in the gaps your government couldn’t fill in the years (see picture above – the unlucky und unsuccessful attempt to the create a government based Digital Identity in Germany).

Now it’s your chance to becoming the long awaited ecosystem of trust.

How can

Digital Trust look like?

One very interesting use case is to supporting 3rd party services with

onbording-, KYC-, registration-, authentication- and authorization-services.

A bank has the necessary customer data and usually a long relationship either. Digitalize these services via OpenAPIs and become an important part of, probably the most important one of a finance platformeconomy,

Compared with Google’s or Facebook’s social login, but with the regulatory quality, acceptance and reputation even the most demanding onboarding processes can be satisfied with. In Germany companies like

YES or

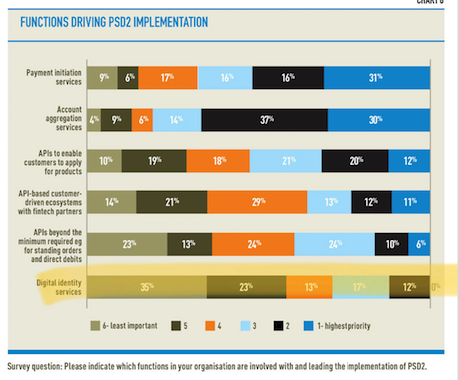

Verimi have already started implementing corresponding services and some banks and insurers have already acknowledged their contribution. But from a platform and CxO perspective this approach is still a very new and less popular one, as this statistic documents.

(Interesting Blog post about Digital Identities –

German)

Another Digital Trust use case is indeed the

good old payment and checkout process. Already a very mature digital process and provided by APIs and many parties (e.g Paypal or Paydirekt), but if provided together with the Digital Identity process banks and insurers could create a vertical touchpoint frame surrounding platform activities and services.

Compared with a room or building where you

‘own’ the save entry and exit. The customer always will pass both.

Fill the room with services and products the customer needs, not necessarily the ones you created, but which helps the customer most.

This is another important aspect of creating an Ecoystem of Trust. A good and recent example is the integration of

Friendsurance into the Deutsche Bank Retail portal.

Deutsche Bank owns the entry, the exit and provides an insurance comparison platform, not the one insurance product. Deuba provides what the customer is looking for, not what serves the bank most – selling the one insurance.

Revitalizing the very old Ecosystems of Trust – the banks and the insurers.

So how can one survive this new ecosystem war?

Fight the trust battle!

Participate and build your own ecosystem and do what you can do best to play a sustainable, prefered and accepted role.

Be the most trusted partner for your customer and support him with (Digital) Trust Services. Base your new ecosystem on trust and fill in the gaps your government couldn’t fill in the years (see picture above – the unlucky und unsuccessful attempt to the create a government based Digital Identity in Germany).

Now it’s your chance to becoming the long awaited ecosystem of trust.

How can Digital Trust look like?

One very interesting use case is to supporting 3rd party services with onbording-, KYC-, registration-, authentication- and authorization-services.

A bank has the necessary customer data and usually a long relationship either. Digitalize these services via OpenAPIs and become an important part of, probably the most important one of a finance platformeconomy,

Compared with Google’s or Facebook’s social login, but with the regulatory quality, acceptance and reputation even the most demanding onboarding processes can be satisfied with. In Germany companies like YES or Verimi have already started implementing corresponding services and some banks and insurers have already acknowledged their contribution. But from a platform and CxO perspective this approach is still a very new and less popular one, as this statistic documents.

So how can one survive this new ecosystem war?

Fight the trust battle!

Participate and build your own ecosystem and do what you can do best to play a sustainable, prefered and accepted role.

Be the most trusted partner for your customer and support him with (Digital) Trust Services. Base your new ecosystem on trust and fill in the gaps your government couldn’t fill in the years (see picture above – the unlucky und unsuccessful attempt to the create a government based Digital Identity in Germany).

Now it’s your chance to becoming the long awaited ecosystem of trust.

How can Digital Trust look like?

One very interesting use case is to supporting 3rd party services with onbording-, KYC-, registration-, authentication- and authorization-services.

A bank has the necessary customer data and usually a long relationship either. Digitalize these services via OpenAPIs and become an important part of, probably the most important one of a finance platformeconomy,

Compared with Google’s or Facebook’s social login, but with the regulatory quality, acceptance and reputation even the most demanding onboarding processes can be satisfied with. In Germany companies like YES or Verimi have already started implementing corresponding services and some banks and insurers have already acknowledged their contribution. But from a platform and CxO perspective this approach is still a very new and less popular one, as this statistic documents.