Kommenden Dienstag treffen sich für ein sehr aktuelles Thema namhafte Vertreter der Versicherungswelt, bunt gemischt aus traditionellen Versicherungsunternehmen und Startups, erstmalig in Köln bei AXA. Der Name

OpenCologne ist hierbei bewusst Programm –

Köln erster Austragungsort und

Open das Leitthema der Veranstaltung.

Mit an Bord sind Vertreter der Zurich, Generali, Talanx, DEVK, Gothaer, Uniqa, Alte Leipziger und AXA, aber auch Startups wie Friendsurance, Schutzklick, Kasko, Element und eine Reihe weiterer Experten.

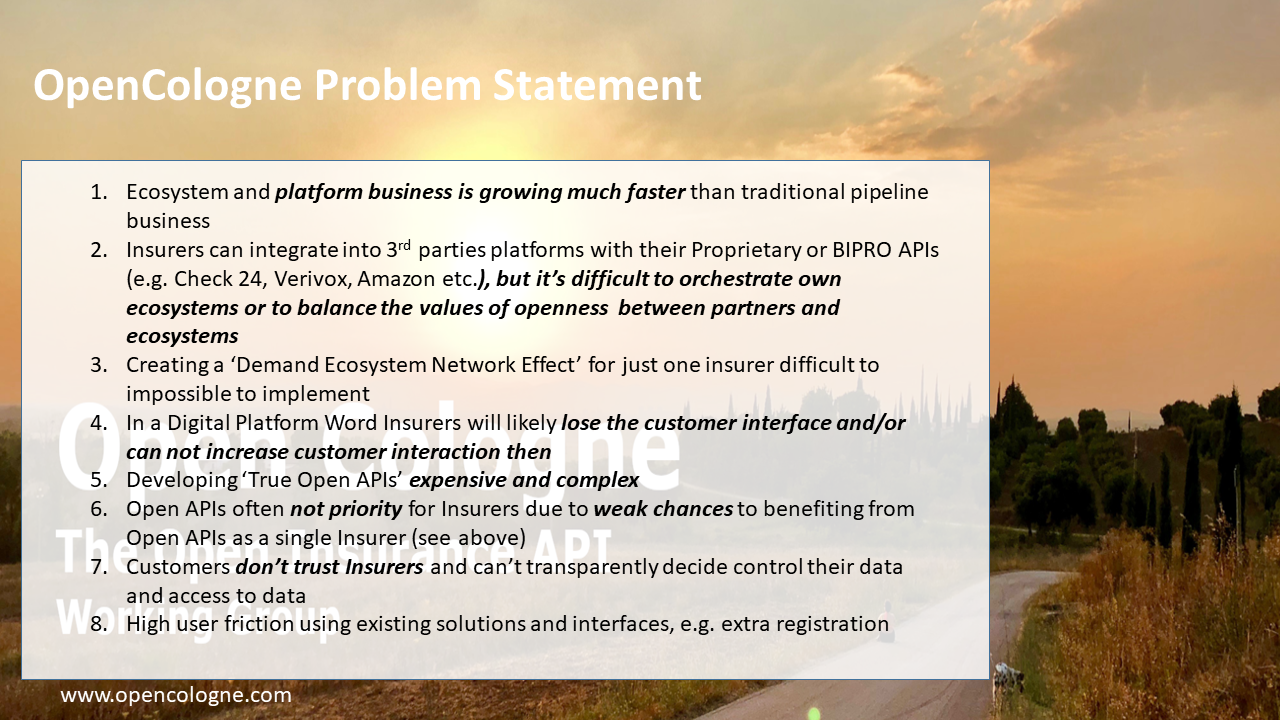

Zielsetzung des ersten Aufeinandertreffen ist die offene, aber durchaus gewollte und zielgerichtete Diskussion offener Standards für vom Kunden kontrollierte, regulierte und grenzenlos einsetzbare B2C APIs:

- Glauben die Teilnehmer daran, dass die Reduktion der Informations-Asymmetrie durch Öffnung ihnen und allen Teilnehmern einen Mehrwert bietet?

- Ist ein gemeinsamer Standard in Summe wertvoller, als proprietäre Offene APIs vom jeweiligen Teilnehmer?

- Finden die teilnehmenden Protagonisten einen gemeinsamen Nenner und ein Verständnis für eine erste Implementierung, für eine API, wie es diese im Bereich von Banken in Deutschland schon lange gibt und ab Ende 2019 auch Europaweit geben wird (PSD2)?

Wie auch schon seit Jahren im Bankenumfeld ist dieses Thema stark polarisierend und wird, je nach Perspektive, in die eine oder andere Richtung schon vorab emotional diskutiert.

Auch ich, als langjähriger Teilnehmer der vielen Banken-API-Diskussionen, bin mir letztendlich noch unschlüssig, ob eine Öffnung und Standardisierung und wenn ja, welcher Grad genau, einen Mehrwert für Kunden und Versicherungen bieten wird. Insofern ist das erste Zusammentreffen auch für mich persönlich und meine Sichten eine gewollte Challenge.

Ich werde unsere, meine Gedanken vorstellen und bin gespannt auf das Feedback, die anschließende Diskussion und den Verlauf.

Wird es am Ende des Tages ein weiteres dieser vielen Austauschmeetings der Versicherungsbranche werden oder doch vielleicht der Startschuss zu einer langen ‘Reise einiger Entwickler, um mit neuen Architekturen und Schnittstellen die Versicherungswelt neu zu vermessen’?

Ich kann es nicht sagen. Aber eines weiß ich aber schon jetzt:

Unser Meetingraum wird voller werden, als gedacht und geplant. Es kann durchaus sein, dass einige Mitstreiter im Stehen die Welt verändern müssen 🙂

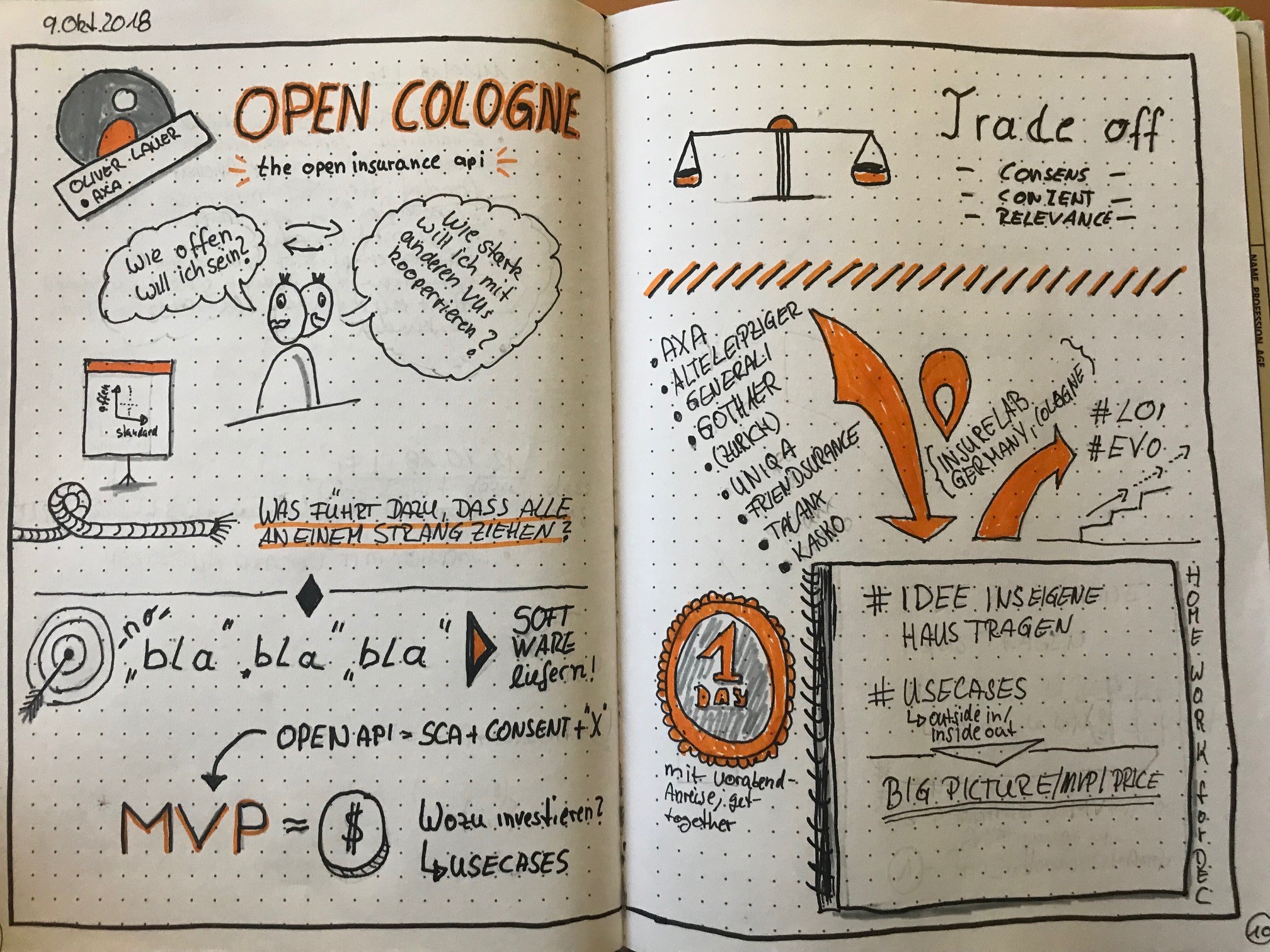

Infos und Gedanken zu OpenCologne:

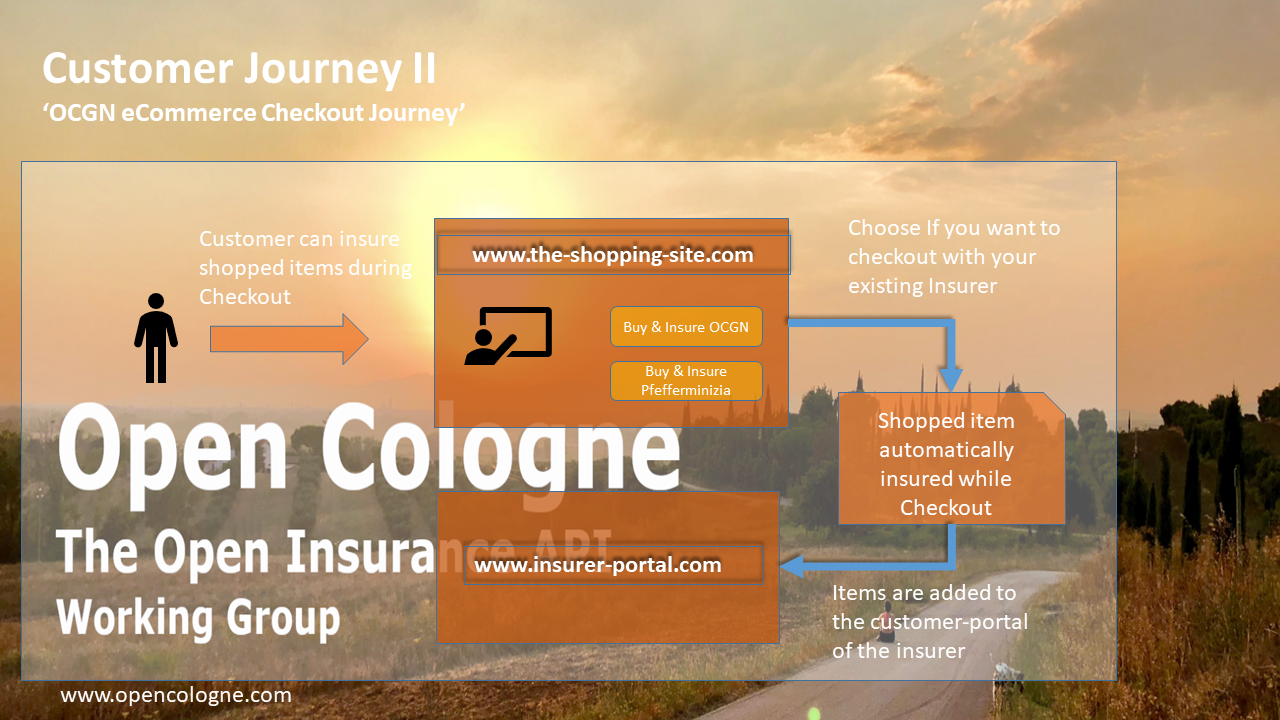

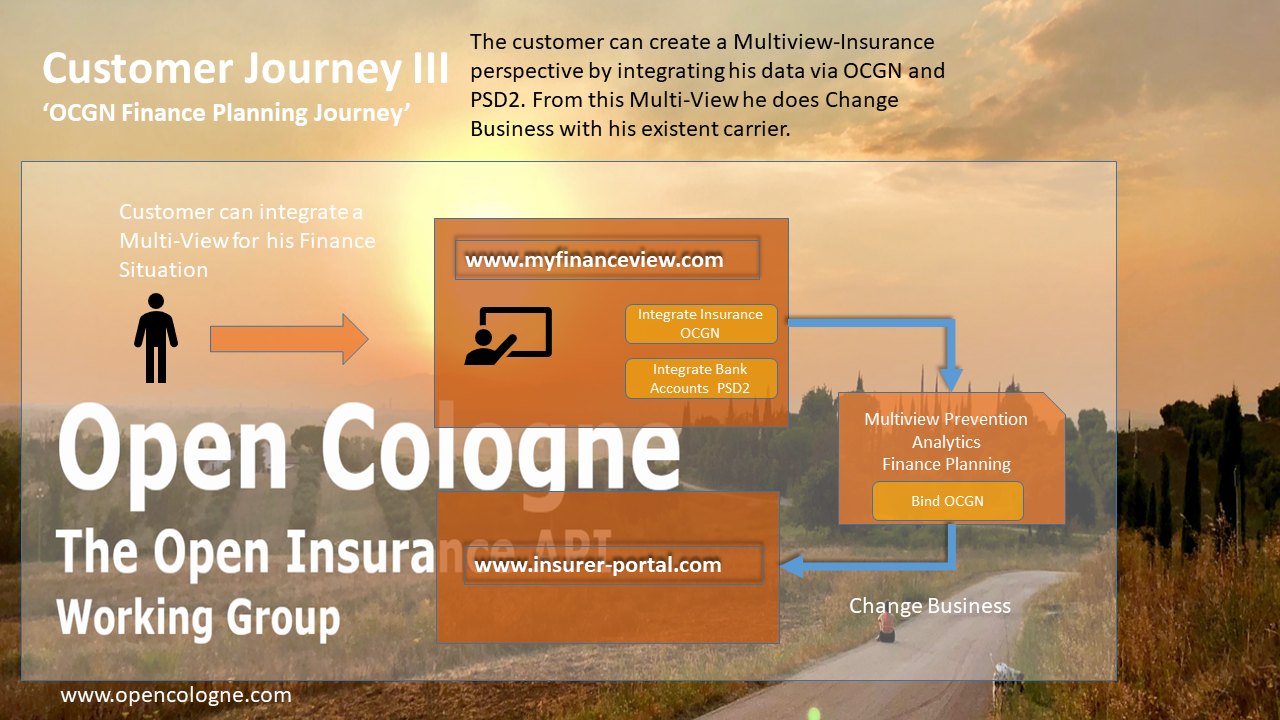

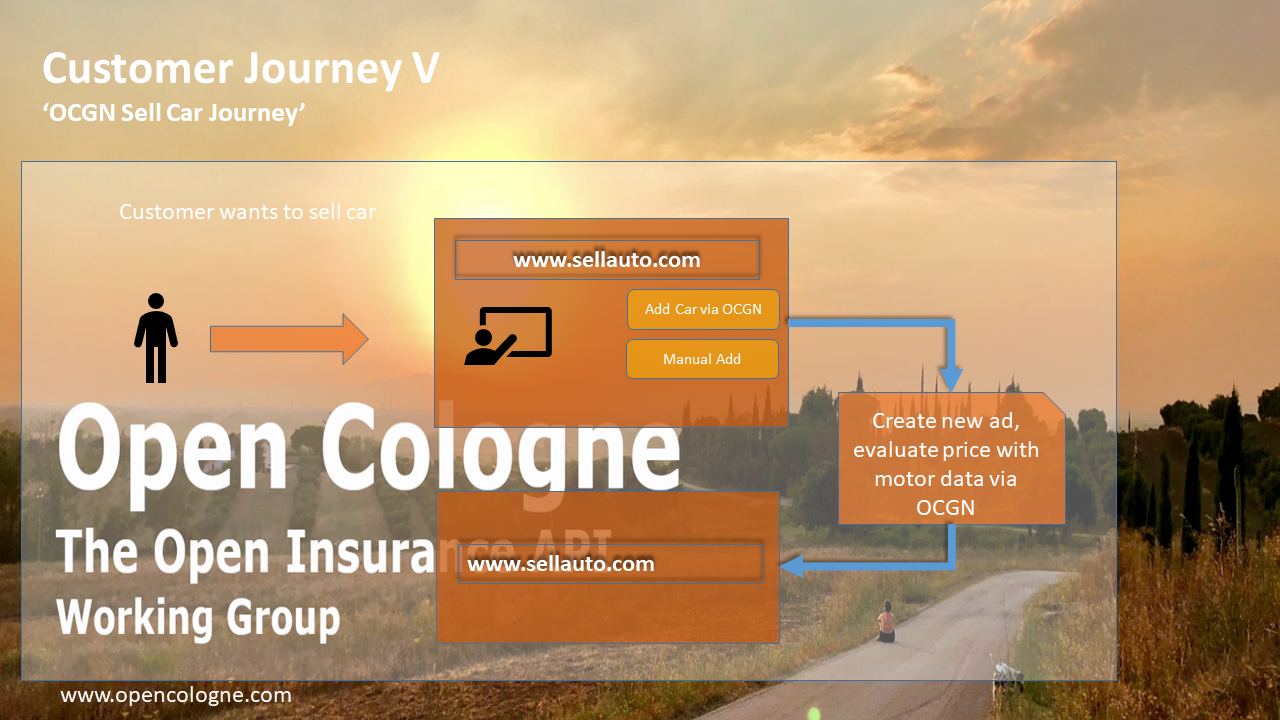

OpenCologne Customer Journeys

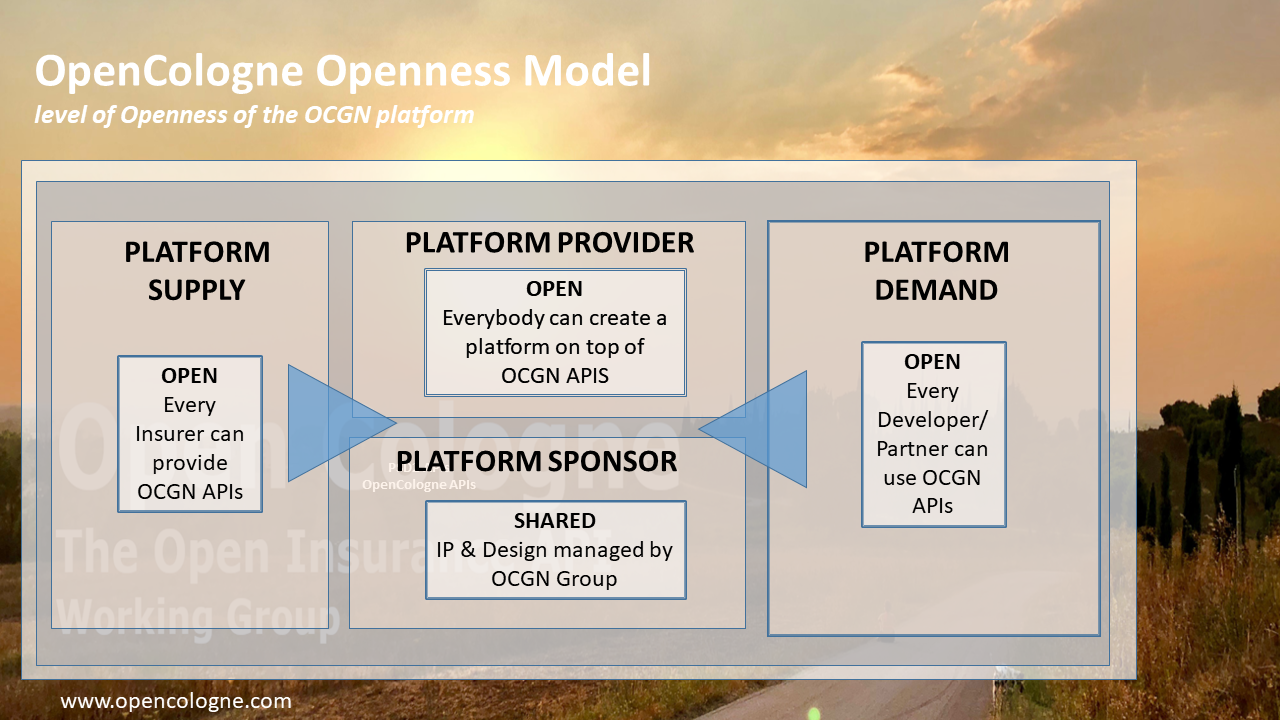

OpenCologne Openness

OpenCologne Agenda

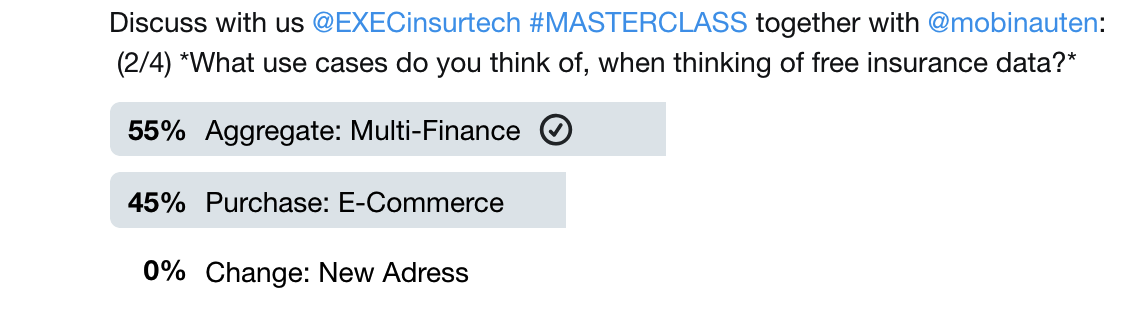

I saw a lot of interesting solutions and ideas. On a high level these could be sorted into one of these three categories:

I saw a lot of interesting solutions and ideas. On a high level these could be sorted into one of these three categories:

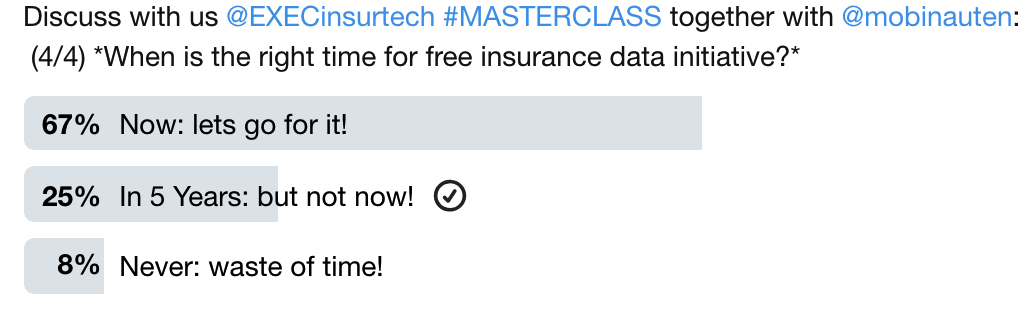

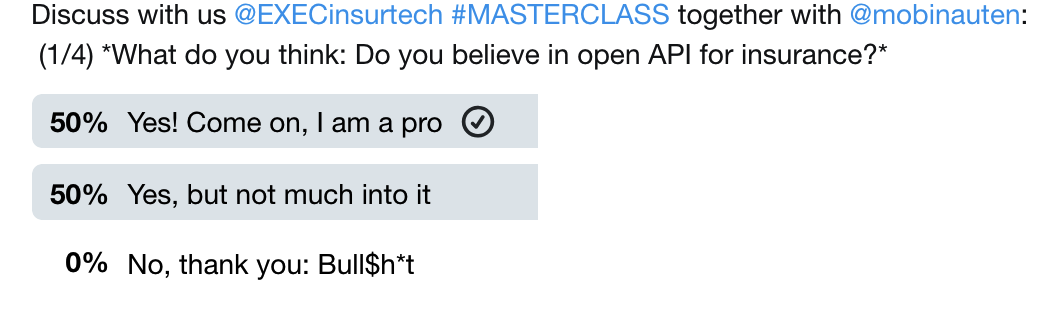

These polls and our classroom results are far from being representative.

But with the solutions I saw at ExecInsurtech, the feedback I received and the discussions I led I believe I see a trend.

And an interesting question remained in the room:

How should/could the existing and traditional world handle and react to it?

These polls and our classroom results are far from being representative.

But with the solutions I saw at ExecInsurtech, the feedback I received and the discussions I led I believe I see a trend.

And an interesting question remained in the room:

How should/could the existing and traditional world handle and react to it?