Architecture follows Strategy. Project follows Architecture.

I would label myself as a ‘

Hybrid Transformer‘ supporting technical and organisational transformations – following the one, given strategy.

Doing it right translates typically to

Architecture and Organisation as a Strategy!

And having worked within this context for quite a while what surprises me most is how badly companies are often prepared for huge transformations.

Although spending two or often three digit sums of Million Euro seldom a clear strategy is defined nor is the base- or target-strategy, -architecture or -organisation with its gaps documented and maintained at the beginning of or even during a project.

After a visionary start companies often activate the ‘Program Auto Pilot’ and focus the technical tasks to migrating the one core to the next.

Usually relying on third parties doing all the rest for you, but don’t really care for the development of your organisation as a whole.

This might work, as a blind date works from time to time, if you find the one or two heroes for your fairy tale, but not very often.

A

As a responsible person for huge transformations I would not only install an Architecture Office or an Architecture Board, hire Solution Architects to act as fire fighters, I would implement, as one of my very first actions, a working Enterprise Architecture Process and Governance in order to control and manage not only my technology challenges, but also my architectural, organisational and strategic ones.

Enterprise Management (

EAM) is a rather mature discipline today. The tools and processes can be helpful and supportive applied carefully.

The most popular one is

TOGAF supported by the

Archimate Modelling Language. And TOGAF and Archimate are not only for techies.

An

ADM with its different viewports is helpful for everyone – from the developer to the CEO.

It constantly should tell you, where you are and where you want to go. And why!

If you start a huge transition program and you don’t find a working Enterprise Architecture with clear vision, business-, architecture-baseline and target models aligned by defined processes and decision boards be very careful and ask necessary questions.

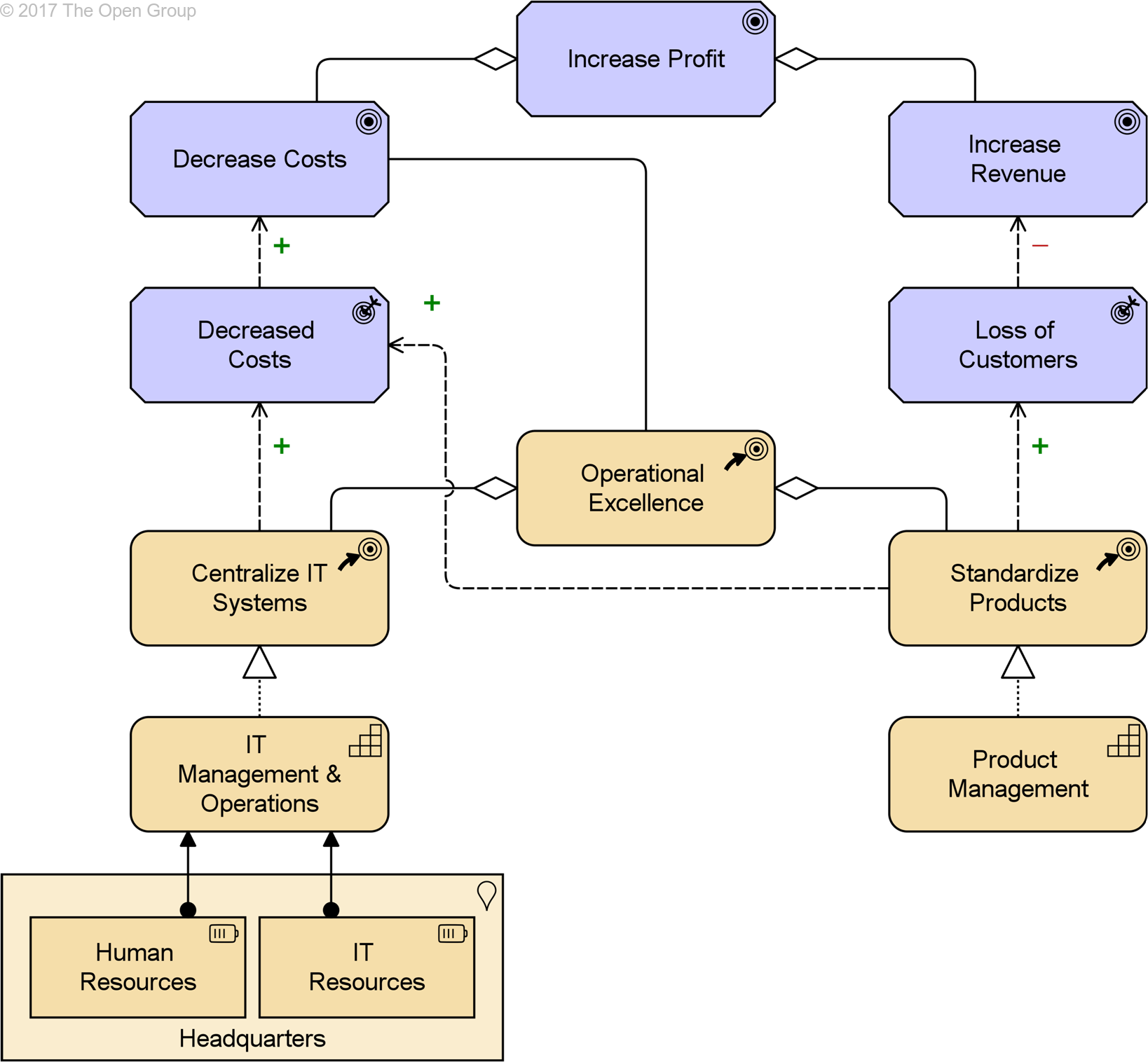

(Strategy as a diagram – Credits to

OpenGroup)

A Blind Date can work, but it typically includes a lot more surprises than other dates.

If you love surprises and firefighting don’t care for Enterprise- Architecture and -Management!

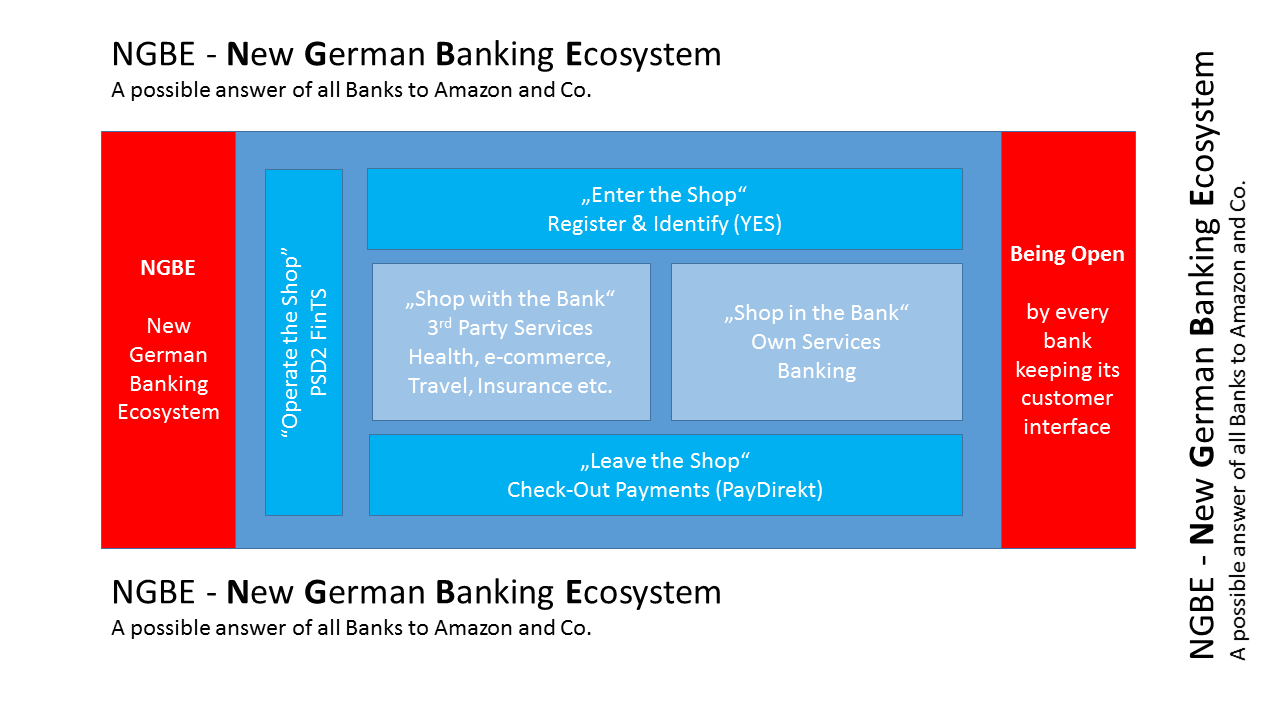

The BerlinGroup tries to changing this by providing one technical API specification. Additionally the BerlinGroup NextGen Implementation also aims at supporting this one interface approach by providing technical solutions or at least concrete specifications for tests and test servers.

Florian and I are member of the BerlinGroup Implementation. We are close to the current developments.

This Open Source Swagger API Technical Spec based on the BerlinGroup specification is one first result.

What we try to achieve with the OpenPSD initiative is to building software based on what we are learning and defining at BerlinGroup.

We would like to build OpenSource software which reflects our activities at BerlinGroup.

Everybody should benefit from OpenPSD and nobody should have to pay for ‘Open’.

The ‘Open’ of Open Banking!

Feel free to contribute, just drop us a mail!

The BerlinGroup tries to changing this by providing one technical API specification. Additionally the BerlinGroup NextGen Implementation also aims at supporting this one interface approach by providing technical solutions or at least concrete specifications for tests and test servers.

Florian and I are member of the BerlinGroup Implementation. We are close to the current developments.

This Open Source Swagger API Technical Spec based on the BerlinGroup specification is one first result.

What we try to achieve with the OpenPSD initiative is to building software based on what we are learning and defining at BerlinGroup.

We would like to build OpenSource software which reflects our activities at BerlinGroup.

Everybody should benefit from OpenPSD and nobody should have to pay for ‘Open’.

The ‘Open’ of Open Banking!

Feel free to contribute, just drop us a mail!

This is ok, as Machine Learning is ok as well, if you know their limitations and risks.

Like Machine Learning a good Gut Instinct needs a lot of data, training and feedback.

If one makes a Gut decision and the data and the training has not been available in the past a Gut decision can have fatal consequences.

Especially senior people and managers often believe their decisions are well trained Gut decisions, but often these aren’t.

Gut decisions without the necessary training and data (creating the necessary neuronal networks) are Fake Gut Instincts and dangerous either.

It’s not easy to decide when one’s Gut Instinct is fake or a good one, but knowing about the differences helps one to being a little more sensitive when pushing your strategy through the organization.

This is ok, as Machine Learning is ok as well, if you know their limitations and risks.

Like Machine Learning a good Gut Instinct needs a lot of data, training and feedback.

If one makes a Gut decision and the data and the training has not been available in the past a Gut decision can have fatal consequences.

Especially senior people and managers often believe their decisions are well trained Gut decisions, but often these aren’t.

Gut decisions without the necessary training and data (creating the necessary neuronal networks) are Fake Gut Instincts and dangerous either.

It’s not easy to decide when one’s Gut Instinct is fake or a good one, but knowing about the differences helps one to being a little more sensitive when pushing your strategy through the organization.

If you want to perform like a startup you must create comparable conditions and environments. And one of the most important parameters , possible the most important one is to operate without legacy.

And legacy in today’s startup and digitalisation context usually means:

IT Legacy.

That said my tip is to replace legacy as radically as possible. Get rid not only of the one or other core system, but possibly rid off most if not all IT systems.

If you want to perform like a startup you must create comparable conditions and environments. And one of the most important parameters , possible the most important one is to operate without legacy.

And legacy in today’s startup and digitalisation context usually means:

IT Legacy.

That said my tip is to replace legacy as radically as possible. Get rid not only of the one or other core system, but possibly rid off most if not all IT systems.

U

U

A

A