Very often people ask what makes Insurtechs or startups more innovative and more successful than traditional incumbents and insurers.

And the answers usually are:

- They can start from scratch

- They don’t have to deal with legacy

- Processes are simple and very agile as company is much smaller with less people

- Governance is very lightweight or even not existing

- People are much more motivated

- People are more skilled

- …

All valid answers.

But today I would like to add another, in my eyes often an even more important reason:

Insurtechs and startups are managed by people, who still apply the necessary technologies, are very hands-on and know the pros and cons of all their architectures and technologies by being a developer or architect or both.

IT managers and decision managers in traditional incumbents and Insurers, even at the lowest level of management, had been technologist at the start of their careers, but usually have lost all their technology skills over the years.

I have been with so many banks and insurers over the last 30 years, but I never met a 40 or 50 years old manager being able to develop with the latest technologies, even not being able to develop with a 15 years old Java stack.

And these guys in a faster than ever technology driven disruptive insurance world have to decide and to manage technology projects and innovation.

How shall and can this work?

Startups work differently – developer, technologists, typically the best developers and architects within a Insurtech or Fintech make the decisions, even the most important ones.

What does this mean for the incumbents?

They have to change their management structure and their processes radically! Smaller teams, self-contained, connected network-like and not hierarchically, managed by the best technologist within the team. Deciding and working autonomously against company’s strategy.

What does this mean for the IT Manager?

The IT Manager always has to question himself and change roles regularly. After a time of pure administrative leadership work he needs to go back to projects in order to make his ‘hands dirty again’. Work again as an architect, developer or project lead within the latest project and retrain himself.

The incumbent and the manager himself should always see the IT manager role as a role for a limited period of time.

If not they will kill innovation and in the long run the company.

So how can one survive this new ecosystem war?

Fight the trust battle!

Participate and build your own ecosystem and do what you can do best to play a sustainable, prefered and accepted role.

Be the most trusted partner for your customer and support him with (Digital) Trust Services. Base your new ecosystem on trust and fill in the gaps your government couldn’t fill in the years (see picture above – the unlucky und unsuccessful attempt to the create a government based Digital Identity in Germany).

Now it’s your chance to becoming the long awaited ecosystem of trust.

How can Digital Trust look like?

One very interesting use case is to supporting 3rd party services with onbording-, KYC-, registration-, authentication- and authorization-services.

A bank has the necessary customer data and usually a long relationship either. Digitalize these services via OpenAPIs and become an important part of, probably the most important one of a finance platformeconomy,

Compared with Google’s or Facebook’s social login, but with the regulatory quality, acceptance and reputation even the most demanding onboarding processes can be satisfied with. In Germany companies like YES or Verimi have already started implementing corresponding services and some banks and insurers have already acknowledged their contribution. But from a platform and CxO perspective this approach is still a very new and less popular one, as this statistic documents.

So how can one survive this new ecosystem war?

Fight the trust battle!

Participate and build your own ecosystem and do what you can do best to play a sustainable, prefered and accepted role.

Be the most trusted partner for your customer and support him with (Digital) Trust Services. Base your new ecosystem on trust and fill in the gaps your government couldn’t fill in the years (see picture above – the unlucky und unsuccessful attempt to the create a government based Digital Identity in Germany).

Now it’s your chance to becoming the long awaited ecosystem of trust.

How can Digital Trust look like?

One very interesting use case is to supporting 3rd party services with onbording-, KYC-, registration-, authentication- and authorization-services.

A bank has the necessary customer data and usually a long relationship either. Digitalize these services via OpenAPIs and become an important part of, probably the most important one of a finance platformeconomy,

Compared with Google’s or Facebook’s social login, but with the regulatory quality, acceptance and reputation even the most demanding onboarding processes can be satisfied with. In Germany companies like YES or Verimi have already started implementing corresponding services and some banks and insurers have already acknowledged their contribution. But from a platform and CxO perspective this approach is still a very new and less popular one, as this statistic documents.

(Interesting Blog post about Digital Identities – German)

Another Digital Trust use case is indeed the good old payment and checkout process. Already a very mature digital process and provided by APIs and many parties (e.g Paypal or Paydirekt), but if provided together with the Digital Identity process banks and insurers could create a vertical touchpoint frame surrounding platform activities and services.

Compared with a room or building where you ‘own’ the save entry and exit. The customer always will pass both.

Fill the room with services and products the customer needs, not necessarily the ones you created, but which helps the customer most.

This is another important aspect of creating an Ecoystem of Trust. A good and recent example is the integration of Friendsurance into the Deutsche Bank Retail portal.

Deutsche Bank owns the entry, the exit and provides an insurance comparison platform, not the one insurance product. Deuba provides what the customer is looking for, not what serves the bank most – selling the one insurance.

Revitalizing the very old Ecosystems of Trust – the banks and the insurers.

(Interesting Blog post about Digital Identities – German)

Another Digital Trust use case is indeed the good old payment and checkout process. Already a very mature digital process and provided by APIs and many parties (e.g Paypal or Paydirekt), but if provided together with the Digital Identity process banks and insurers could create a vertical touchpoint frame surrounding platform activities and services.

Compared with a room or building where you ‘own’ the save entry and exit. The customer always will pass both.

Fill the room with services and products the customer needs, not necessarily the ones you created, but which helps the customer most.

This is another important aspect of creating an Ecoystem of Trust. A good and recent example is the integration of Friendsurance into the Deutsche Bank Retail portal.

Deutsche Bank owns the entry, the exit and provides an insurance comparison platform, not the one insurance product. Deuba provides what the customer is looking for, not what serves the bank most – selling the one insurance.

Revitalizing the very old Ecosystems of Trust – the banks and the insurers.

For an IT guy the last ten years have been very boring ones often as most IT Euros spent were regulation motivated.

The newest ones for example are

For an IT guy the last ten years have been very boring ones often as most IT Euros spent were regulation motivated.

The newest ones for example are

These kind of vertical ecosystems exist since decades – mutual societies and comparable organisations – but with the digital revolution currently happening everywhere there’s a new chance to reinvent and even to massively extend this model far beyond what was possible before.

And this is a chance for the old incumbents, the old banks and insurers to beat the GAFAs and all other coming platform revolutionaries and newbies on their home-turf.

They know their customers, they have build trust and relationship over the century. Now it’s time to modernize their houses and to copy the digital and platform services approaches. And to profile these much better than the global horizontal providers can.

You don’t need to own the product, you need to ‘own’ the customer and to provide trusted services via modern, simple and fast technologies. In the future you will very likely make more revenue with platform services and network effects than with a traditional approach as these

These kind of vertical ecosystems exist since decades – mutual societies and comparable organisations – but with the digital revolution currently happening everywhere there’s a new chance to reinvent and even to massively extend this model far beyond what was possible before.

And this is a chance for the old incumbents, the old banks and insurers to beat the GAFAs and all other coming platform revolutionaries and newbies on their home-turf.

They know their customers, they have build trust and relationship over the century. Now it’s time to modernize their houses and to copy the digital and platform services approaches. And to profile these much better than the global horizontal providers can.

You don’t need to own the product, you need to ‘own’ the customer and to provide trusted services via modern, simple and fast technologies. In the future you will very likely make more revenue with platform services and network effects than with a traditional approach as these

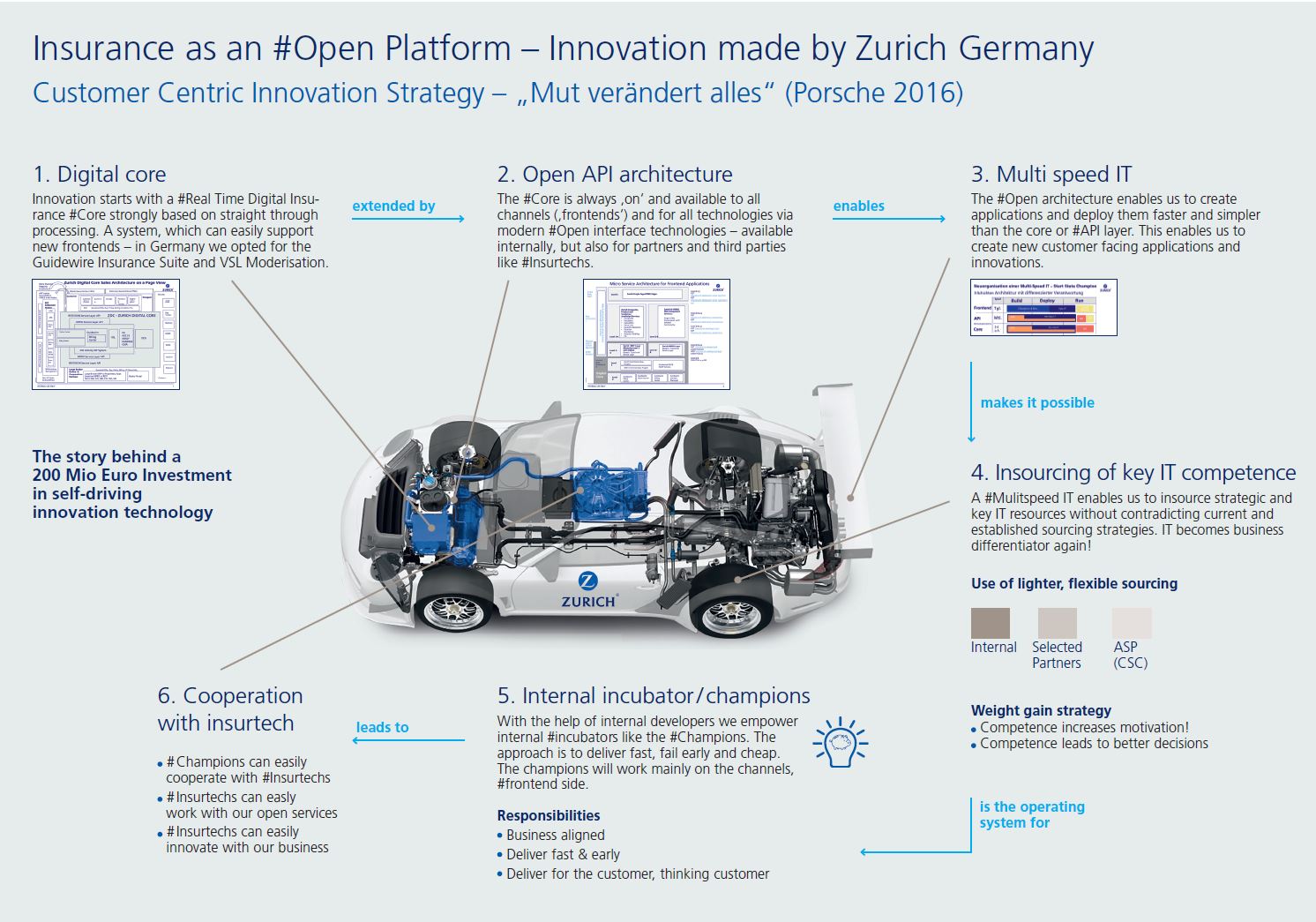

Zurich Insurance in Germany really surprised me. It was a much better experience than expected. I learned if the board members and managers exactly know what you want to do and decide fast and precisely even big projects like this transformation don’t fail.

Transparency in transformation is king.

We will all meet again, I’ sure.

Oliver@Zurich

Zurich Insurance in Germany really surprised me. It was a much better experience than expected. I learned if the board members and managers exactly know what you want to do and decide fast and precisely even big projects like this transformation don’t fail.

Transparency in transformation is king.

We will all meet again, I’ sure.

Oliver@Zurich

Usually an Insurance just sells a promise.

A promise to pay in the case of a claim. It’s neither a product in a traditional sense nor is this really a security service.

But most Insurance companies claim since decades to sell security and safety. Now AXA with Wayguard really delivers security without forcing the user to being or becoming an AXA insurance customer.

I assume it’s not easy to convince your board members to invest money in ideas like Wayguard, where it’s still difficult to measure success and thus its influence on customer gains and BOP.

But the AXA board believed and still believes in an approach like this – I think a very smart and courageous move.

And the way the AXA team with its head Albert Dahmen identified the final idea is also worth talking about:

In an interview approach the AXA team was on the streets asking ordinary people what could make their day to day life more secure. They did not ask for insurance products, even did not present themselves as insurance employes.

And after days and weeks of interviews one of the interviewed answered: ‘I always call my boyfriend when I have to pass dark und unpleasant areas on my way home!’. And this answer was the birth of Wayguard, Albert Dahmen commented .

Usually an Insurance just sells a promise.

A promise to pay in the case of a claim. It’s neither a product in a traditional sense nor is this really a security service.

But most Insurance companies claim since decades to sell security and safety. Now AXA with Wayguard really delivers security without forcing the user to being or becoming an AXA insurance customer.

I assume it’s not easy to convince your board members to invest money in ideas like Wayguard, where it’s still difficult to measure success and thus its influence on customer gains and BOP.

But the AXA board believed and still believes in an approach like this – I think a very smart and courageous move.

And the way the AXA team with its head Albert Dahmen identified the final idea is also worth talking about:

In an interview approach the AXA team was on the streets asking ordinary people what could make their day to day life more secure. They did not ask for insurance products, even did not present themselves as insurance employes.

And after days and weeks of interviews one of the interviewed answered: ‘I always call my boyfriend when I have to pass dark und unpleasant areas on my way home!’. And this answer was the birth of Wayguard, Albert Dahmen commented . How WayGuard works is detailed on the WayGuard

How WayGuard works is detailed on the WayGuard