Nice, but how can that look like in a real world’s scenario?

A lot of articles in our blog deal with platform and open API on a strategic level. We have talked a lot about them in the past. Many decision makers and IT people didn’t ever see an actual platform working in their businesses. We almost every time point to GAFA to demonstrate how platforms can work. But people want to know how to tackle this technological challenge and where to start in their actual IT scenario.

- How can a platform look like from a technical perspective?

- Which different APIs are we going to provide?

- How do we create APIs? How do we secure them?

- How can we manage service versioning as services may evolve over time?

- How can we manage service provisioning and limitations?

- Can I do API-based batch jobs and batch job control as well?

Well, there is a place where I could see how all these questions have got at least some practical answers which seem to be working out somehow: I played around with salesforce’s platform a bit.

Salesforce Trailhead

Salesforce is known as a cloud-based CRM solution in town, but technically it is much more than this. You can create and run every kind of business App on Salesforce’s platform. Many things like IoT, Artificial Intelligence and Big Data services come for free which you can use on top.

In trailhead, salesforce’s training platform where you can find tons of different technical and business tutorials (Trails) around Salesforce and CRM, I registered and started some specific trainings about platform and open API.

The good thing about these “trails” is that they often come with some hands-on sessions where you can really create technical stuff. You are able to see immediately how your results work on a training sandbox salesforce platform which has been created for you during registration.

The other thing which I found amazing is that you can start nearly everywhere you want to become familiar with the platform. I decided to start with Open API, IoT and Mobile Application Development for the platform.

But up to now I really enjoyed this gamification style of trailhead most!

For IT guys in Particular …

Yes, you have to be an IT guy with at least some development background to get through those trails. But if you have that background you will get a very good idea about how an Open API paradigm practically can look like very quickly. If you want to see some real world’s IoT scenarios, no problem. You can even build one yourself too.

In Salesforce there are a lot of different APIs. Every business object and even custom objects which you have created yourself are available via a REST API. There is a Metadata API for customization, a Bulk API for mass data operations. It has built in security mechanisms based on standards like OAuth 2.0. It supports synchronous and asynchronous calls. Versioning and Access limitations are considered out of the box as well.

As long as you develop stuff on the platform or access exposed APIs, you even do not need to install an IDE. All stuff you need (REST Workbench, Development Environment) come with that platform itself. To play with the SOAP API I had to install SOAP UI. For Mobile App development you need stuff like node, npm, git and cordova and some additional salesforce tools. That’s it.

Happy End?

I am not here to make advertising for Salesforce. Of course, Salesforce will definitely have its own pitfalls as well. This is not about “They introduced Salesforce and they lived happily ever after!”. Stuff like this may also be available on ther vendor’s plattforms like SAP or IBM.

But my message to all those people who has to deliver results on platforms, Open API and all the other 4.0 topics like IoT, Big Data and Artificial Intelligence is to take a few hours and play around with salesforce’s offerings on trailhead. You definitely will get some new impulses for your every day’s work. At least you can see how others have solved issues that you are thinking about as well. And for all of you who want to see some actual use cases of open API beyond GAFA it is really worth it.

You can have a look at my

trailhead profile to see what I am talking about.

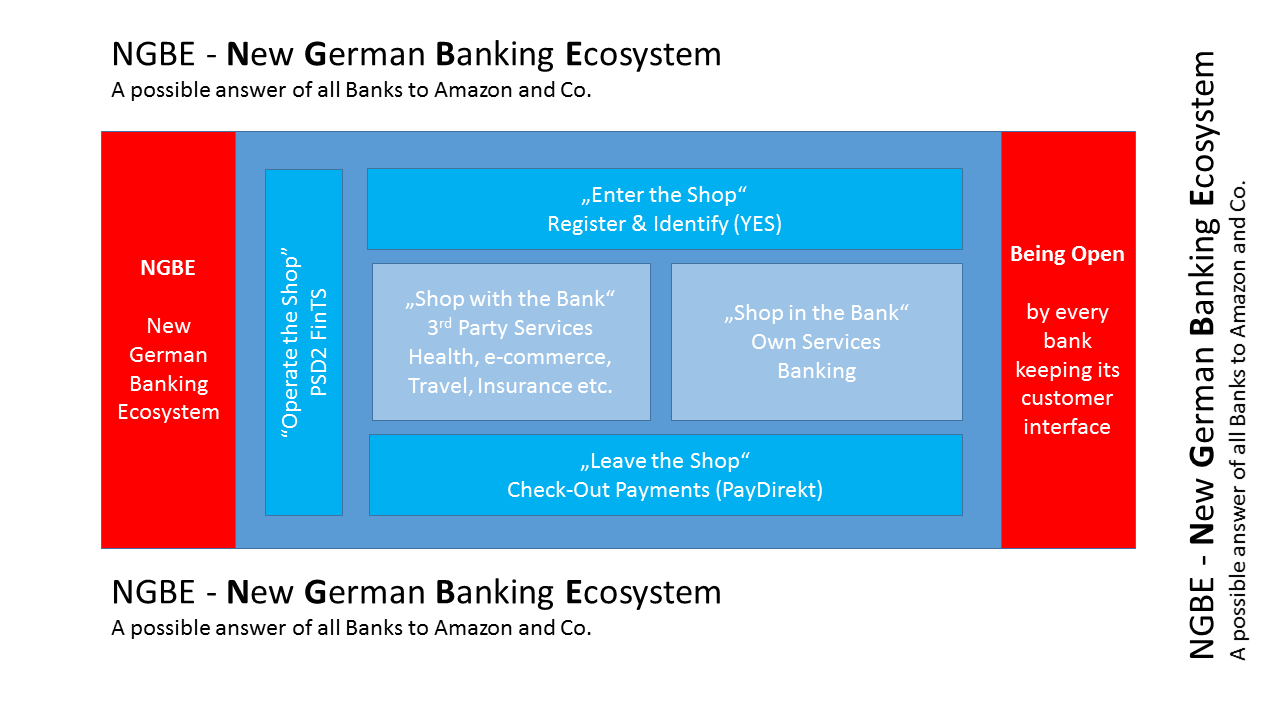

If focussing on a B2B2C business model one can also power the partner by banking enriched Insurtech and mixed banking and insurance capabilities.

All of this will be more or less standardized, available via API and very likely as ‘free lunch’. And if not standardized via BerlinGroup API e.g. then at least a lot of tech API banking aggregators and providers like Figo and others will cover the different API specifications.

From my view it has never been easier to do banking and to combining banking with Insurtech by becoming a BankingInsurtech company.

And to transforming to a tech enabled B2BC financial full service carrier.

The market is not sleeping. Companies and Startups are already working. Archimede is just one example.

There also some OpenSource projects out there implementing OpenBanking APIs, like the one from OpenPSD based on BerlinGroup specification,

If focussing on a B2B2C business model one can also power the partner by banking enriched Insurtech and mixed banking and insurance capabilities.

All of this will be more or less standardized, available via API and very likely as ‘free lunch’. And if not standardized via BerlinGroup API e.g. then at least a lot of tech API banking aggregators and providers like Figo and others will cover the different API specifications.

From my view it has never been easier to do banking and to combining banking with Insurtech by becoming a BankingInsurtech company.

And to transforming to a tech enabled B2BC financial full service carrier.

The market is not sleeping. Companies and Startups are already working. Archimede is just one example.

There also some OpenSource projects out there implementing OpenBanking APIs, like the one from OpenPSD based on BerlinGroup specification,

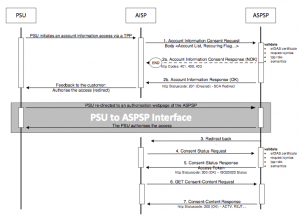

[Source: Berlin Group's Implementation Guidelines]

[Source: Berlin Group's Implementation Guidelines]

This is ok, as Machine Learning is ok as well, if you know their limitations and risks.

Like Machine Learning a good Gut Instinct needs a lot of data, training and feedback.

If one makes a Gut decision and the data and the training has not been available in the past a Gut decision can have fatal consequences.

Especially senior people and managers often believe their decisions are well trained Gut decisions, but often these aren’t.

Gut decisions without the necessary training and data (creating the necessary neuronal networks) are Fake Gut Instincts and dangerous either.

It’s not easy to decide when one’s Gut Instinct is fake or a good one, but knowing about the differences helps one to being a little more sensitive when pushing your strategy through the organization.

This is ok, as Machine Learning is ok as well, if you know their limitations and risks.

Like Machine Learning a good Gut Instinct needs a lot of data, training and feedback.

If one makes a Gut decision and the data and the training has not been available in the past a Gut decision can have fatal consequences.

Especially senior people and managers often believe their decisions are well trained Gut decisions, but often these aren’t.

Gut decisions without the necessary training and data (creating the necessary neuronal networks) are Fake Gut Instincts and dangerous either.

It’s not easy to decide when one’s Gut Instinct is fake or a good one, but knowing about the differences helps one to being a little more sensitive when pushing your strategy through the organization.